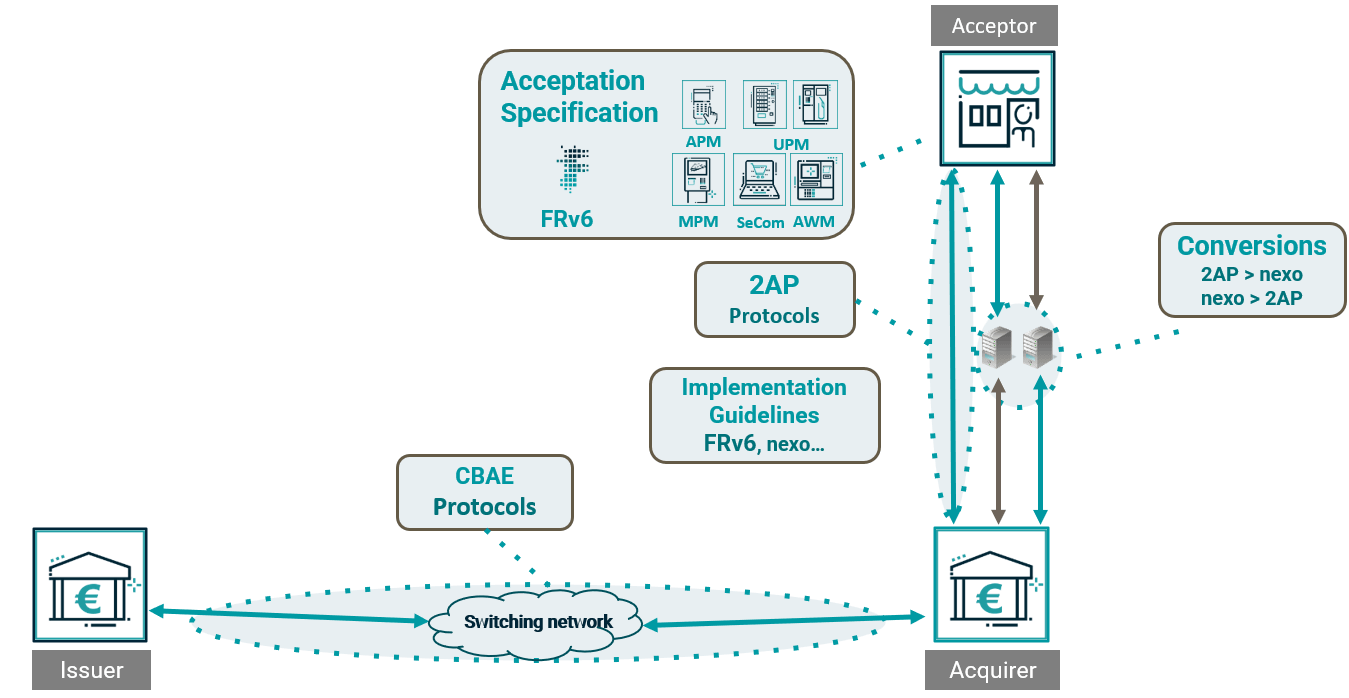

FRv6 Specification

The specifications and protocols of FrenchSys cover the entire processing of a payment transaction, from from payment acceptance by the merchant through the processing by the acquirer until the issuer.

Acceptance

FRv6 : The Reference Standard for Payment Acceptance

The FRv6 acceptance frameworks, developed by FrenchSys, are essential standards in the payments industry. They ensure the smooth and secure processing of card transactions across all acceptance points. Thanks to their compatibility with the seven main payment schemes used in France, they provide a single, centralised solution for merchants and operators.

Key advantages include :

- Flexible and configurable frameworks, adaptable to the specific requirements of each payment scheme

- A consistent payment experience, ensuring ease of use for customers regardless of the merchant

- Simplified connectivity to all French acquirers, through an interface based on the 2AP protocols

Manuals Adapted to Each Payment Environment

Attended Payment Manual (APM) – In-store transactions

The Attended Payment Manual (APM), formerly MPE, defines the rules for accepting proximity payments on payment terminals, both contact and contactless.

The FRv6 version of APM introduces important features such as :

- Online PIN

- Removal of systematic receipt printing

- Donations and tips management

- Additional enhancements to improve the payment experience.

Unattended Payment Manual (UPM) – Payments on automated devices

The Unattended Payment Manual (UPM), formerly MPA, specifies transactions performed on unattended payment terminals, both contact and contactless.

Typical use cases include :

- Highway tolls

- Fuel dispensers (AFDs)

- Electric vehicle charging stations

Like the APM, the FRv6 version of UPM introduces key capabilities such as Online PIN and the removal of mandatory receipt printing.

Secure E-commerce Manual (SEcoM) – Secure online payments

The Secure E-commerce Manual (SEcoM), formerly MPADS, defines the functional requirements and transaction flows for e-commerce payments.

SEcoM relies on EMV 3-D Secure technology, helping online merchants reduce fraud risks through strong customer authentication.

The FRv6 version of SEcoM introduces features such as :

- CIT and MIT transaction chaining

- New functionalities including 3RI

- Partial captures

Mobility Payment Manual (MPM) – Payments on transport validators

The Mobility Payment Manual (MPM), formerly MPAT, defines the requirements for contactless electronic payments on transport validators.

The manual describes the process of :

- Open Payment systems

- Single Ticket Transaction systems

Its main objective is to provide a single acceptance solution focusing on interoperability, risk management, and efficient passenger flow in transport environments.

ATM Withdrawal Manual (AWM) – Secure withdrawals

The ATM Withdrawal Manual (AWM), formerly MRA, defines the acceptance rules for cash withdrawals at ATMs.

It enables the implementation of withdrawal solutions compliant with interbank and security requirements for EMV contact and contactless transactions, based on standards from EMVCo.

Protocols

Acceptor Acqueror Protocol (2AP)

The 2AP protocol (formerly CB2A) is a key standard for card payment processing in France, developed to meet the specific needs of the national market by FrenchSys.

First introduced in the 1990s, this protocol was designed to standardise exchanges between payment solutions and acquirer systems, ensuring optimal interoperability among the different stakeholders in the payment ecosystem.

The 2AP protocol governs the data exchanges required for several core processes :

- Payment authorization

- Data capture (capture transactions for clearing)

- POI configuration

It therefore ensures the smooth execution of transactions whether they occur in-store, on unattended devices, or online.

Over time, 2AP has evolved to integrate advanced functionalities that reflect the rapid evolution of payment technologies :

- Adoption of EMVCo technologies (Europay, Mastercard, Visa)

- Introduction of contactless payments

- Transaction chaining

This adaptability allows the protocol to remain relevant while delivering a reliable, secure, and simplified user experience.

The 2AP protocol is scheme-agnostic, meaning it supports several card networks including American Express, Cartes Bancaires (CB), Discover, JCB, Mastercard, UnionPay (UPI), and Visa.

This flexibility :

- Simplifies system integration for merchants and acquirers

- Reduces operational costs linked to managing multiple protocols

- Ensures consistent transaction processing regardless of the card used

Additionally, 2AP is supported by all major French acquirers, facilitating communication with their systems and significantly reducing costs for merchants and payment service providers.

By standardising and simplifying payment processes, 2AP strengthens trust among consumers and merchants within the French electronic payments ecosystem.

CBAE Protocol (Acquirer–Issuer)

The CBAE protocol ensures interbank interoperability and authorisation data exchange between acquirers and issuers.

It acts as a bridge between :

- the 2AP Authorisation protocol, used between acceptors and acquirers

- and the protocols of the various international payment schemes used between acquirers and issuers.

Continuously evolving, CBAE incorporates new payment scheme requirements each year. Updated specifications are published on January 31 each year, with implementation scheduled for June.

CBAE also integrates the latest regulatory developments, including compliance with Revised Payment Services Directive (PSD2) and Strong Customer Authentication (SCA).

By ensuring smooth and efficient interconnection between the different payment stakeholders, the CBAE protocol remains a critical component of the French payment infrastructure.